An opportunity to transform the Argentinean energy system

03.08.2021

Additional Authors: María Paz Cristofalo and Alejandro Haim

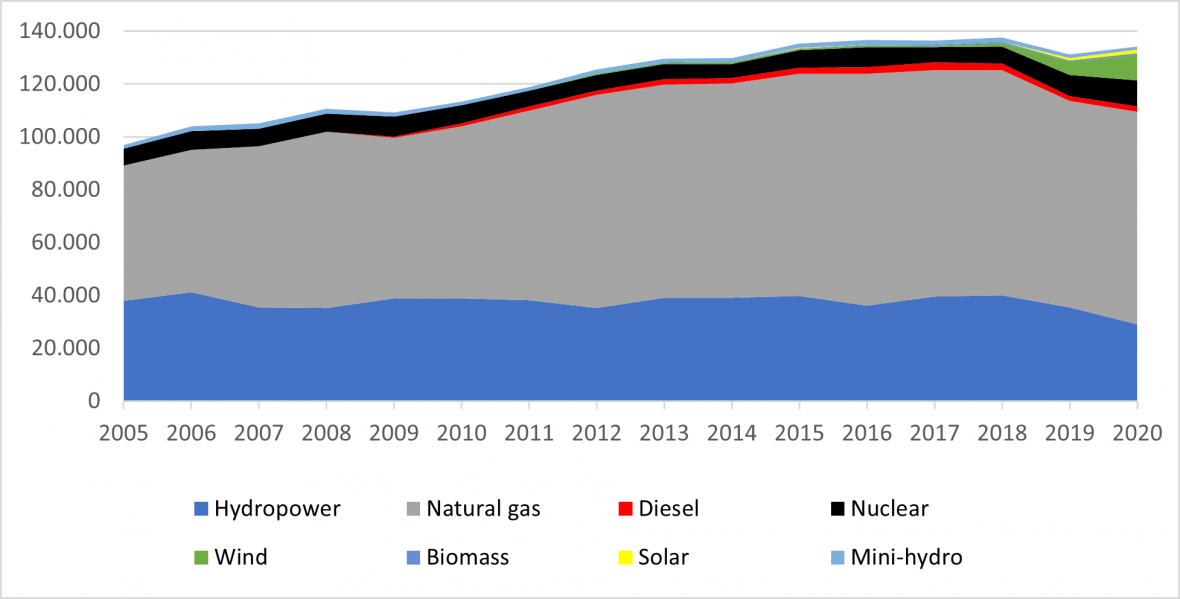

The Argentinean electricity sector remains concentrated in a few actors and is highly dependent on fossil fuels. In 2020 natural gas provided 60% of electricity production, large hydropower plants 22%, and nuclear energy 7.5% (Figure 1). In an oligopolist electricity sector, public companies control nuclear and the main hydropower plants, and a few private companies own the gas-powered stations. Installed capacity of renewables (wind, solar PV, biomass, and mini hydro) has increased in the last few years, providing 9.5% of total power generation in 2020, and the official target is to achieve at least 20% by 2025.

The deployment of renewable energy has been supported by an auction system known as RENOVAR. Through this programme, large wind farms and some solar PV parks flourished in regions with the most appropriate climatic conditions (wind in Patagonia, and sun in the north and west). However, two substantial obstacles threaten the realisation of new, large renewable energy projects in the nearer future: the saturation of transmission lines, associated with a lack of new investment; and insufficient project funding, due to the poor macroeconomic situation. The impacts of the COVID-19 pandemic have exacerbated Argentina’s macroeconomic problems, led to job losses, and increased energy poverty for millions of families. In that context, we discuss the opportunities and barriers to supporting micro-scale renewable energy projects, which can directly benefit families and small businesses throughout the country.

Figure 1: Annual electricity generation (GWh) by source. Data: CAMMESA 2021.

Argentina lags behind many of its neighbours in renewable distributed generation (DG) in both PV panels for electricity production and solar collectors for warm water. The administrative complexity of the RENOVAR programme hinders the participation of new small- and micro-scale electricity producers, and the legal status of prosumer was only introduced to national legislation in 2018. However, more and more stakeholders are showing interest in DG. At a workshop held in June 2021, participants highlighted several advantages and potential benefits of DG in the wake of the COVID-19 pandemic:

a) Technical: relieving pressure on the electrical transmission networks and contributing to maintaining electricity supply during peak hours;

b) Economic: reducing electricity bills, creating efficiency gains, while requiring less project funding;

c) Environmental: reducing carbon emissions and air pollution;

d) Socio-political: increasing participation and integration of new actors and facilitating energy access in remote rural areas.

How can Argentina take advantage of DG during its recovery from the pandemic? Which technologies are the most appropriate? In the following, we share key points discussed during the workshop, including a techno-economic analysis of solar collectors, the progress on implementing the new law promoting DG, and the possible role of green microfinance in increasing access and participation.

Solar thermal collectors: slow diffusion in a sunny country

Argentina is a vast and geographically diverse country, spanning around 3700 km from the northern Jujuy province to the southern Tierra del Fuego. Consequently, there are substantial differences in temperature, wind, and global and direct solar radiation across the country.

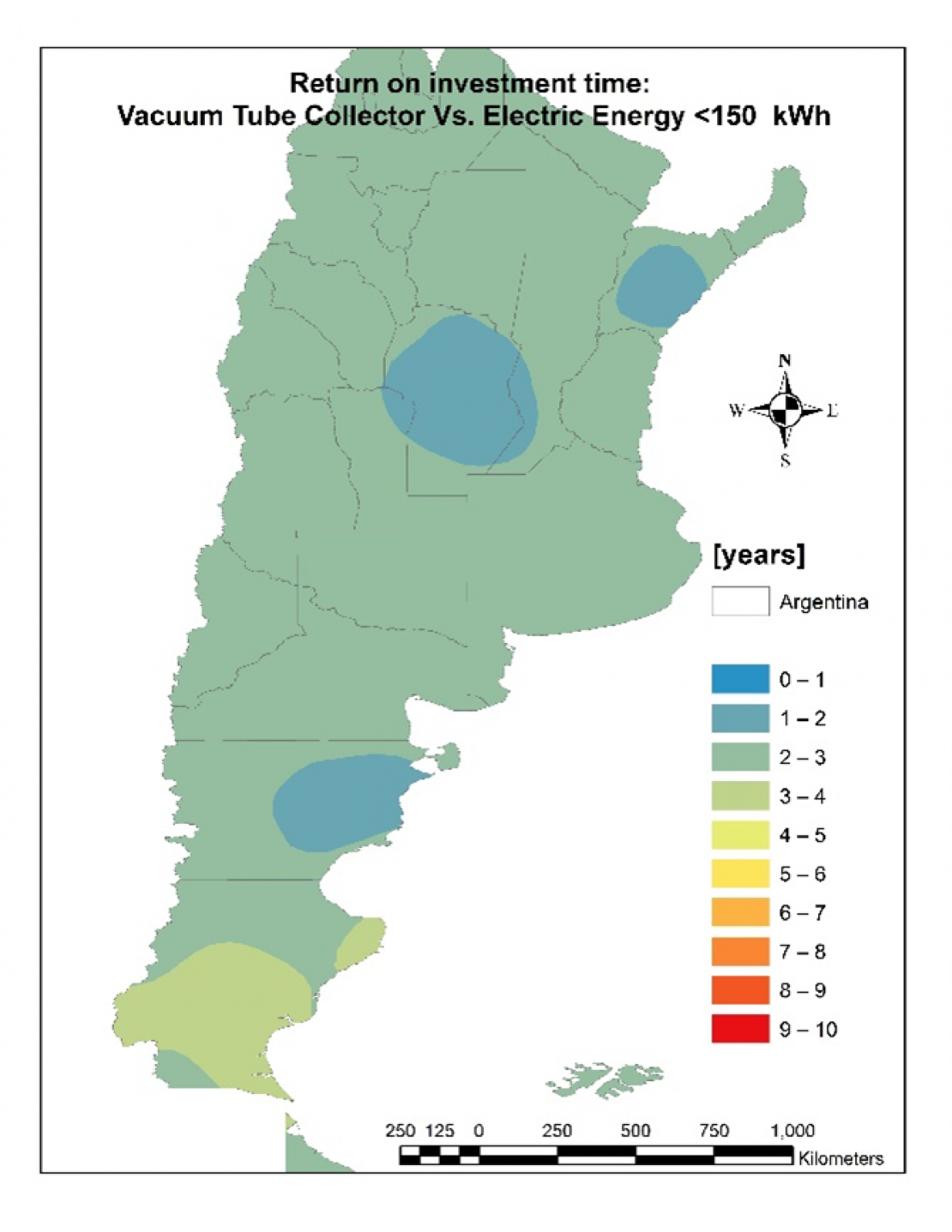

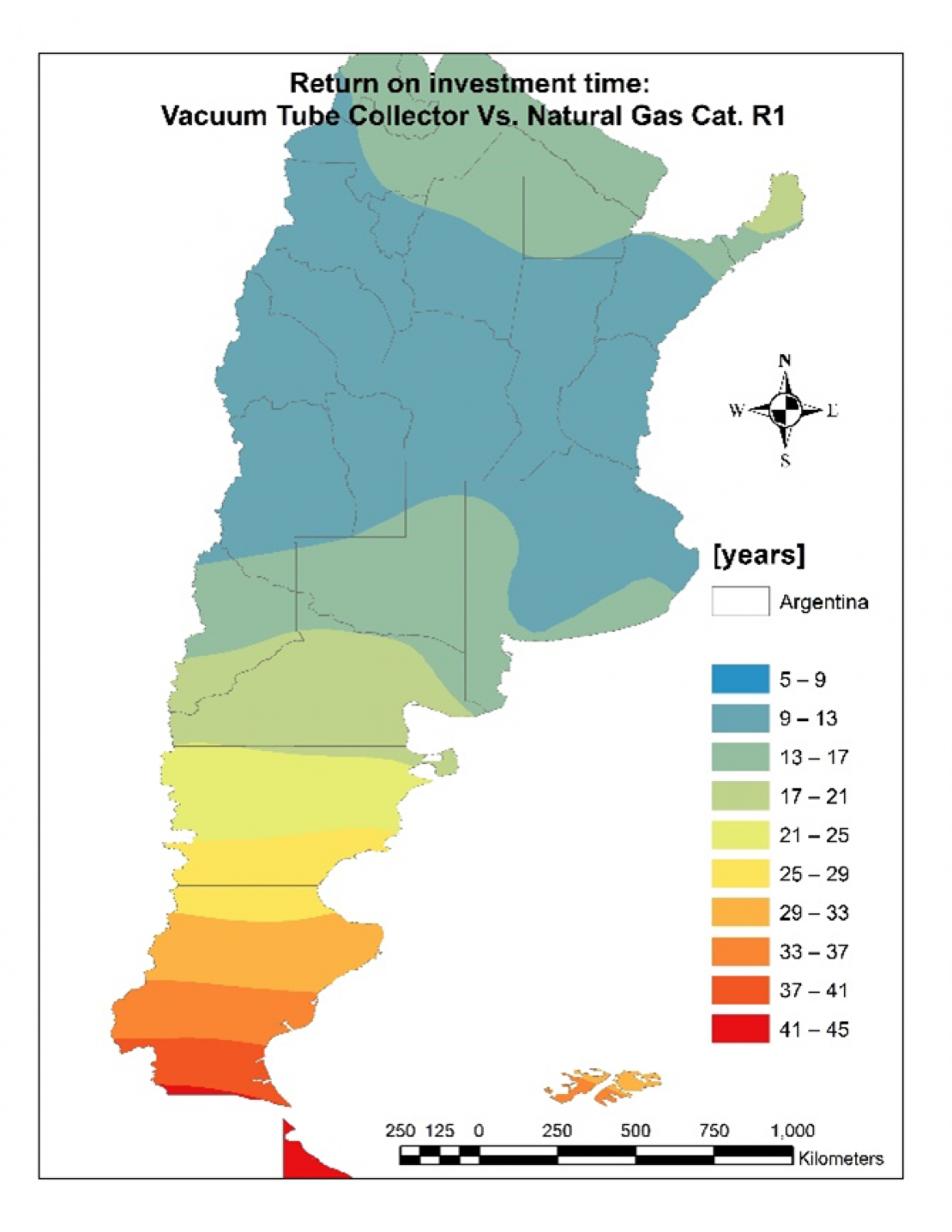

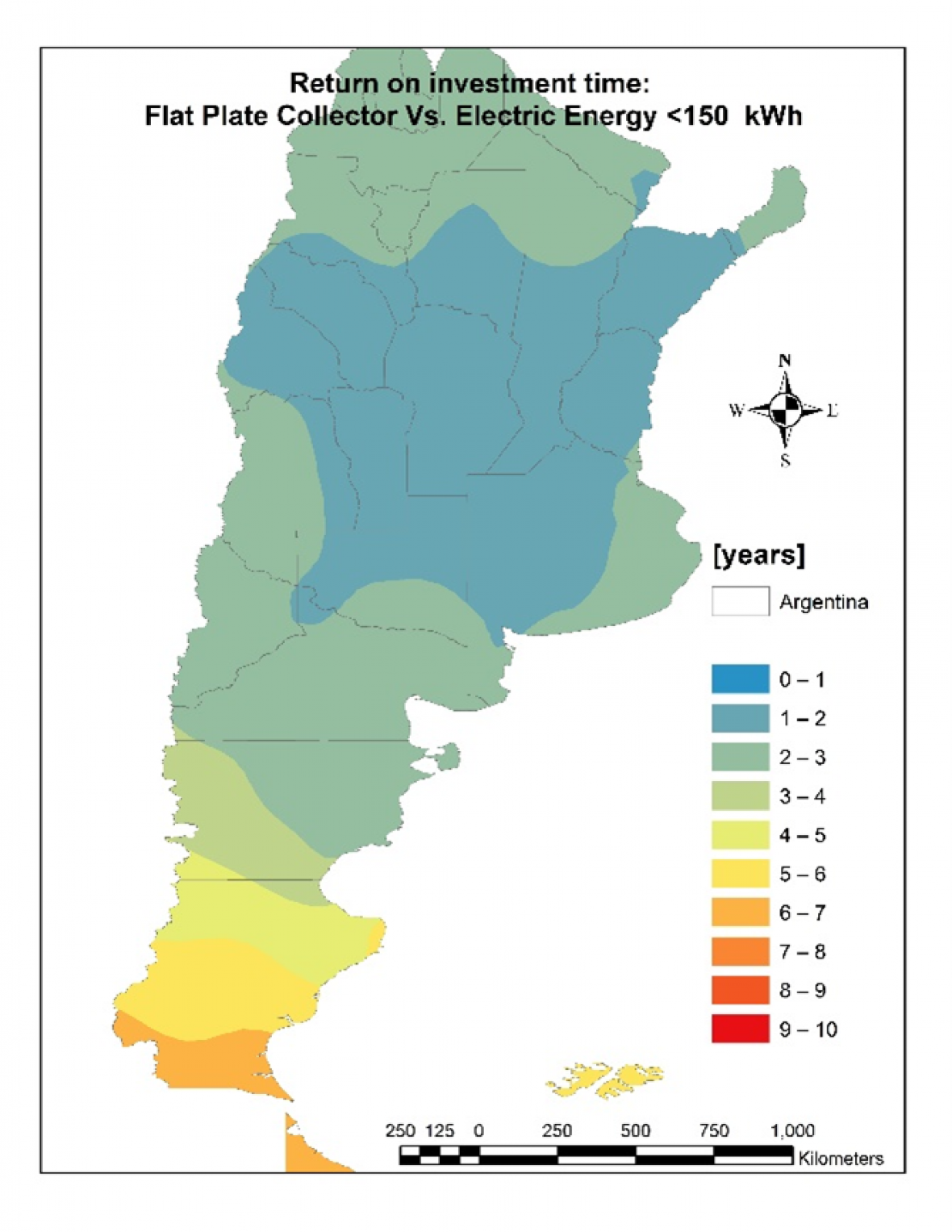

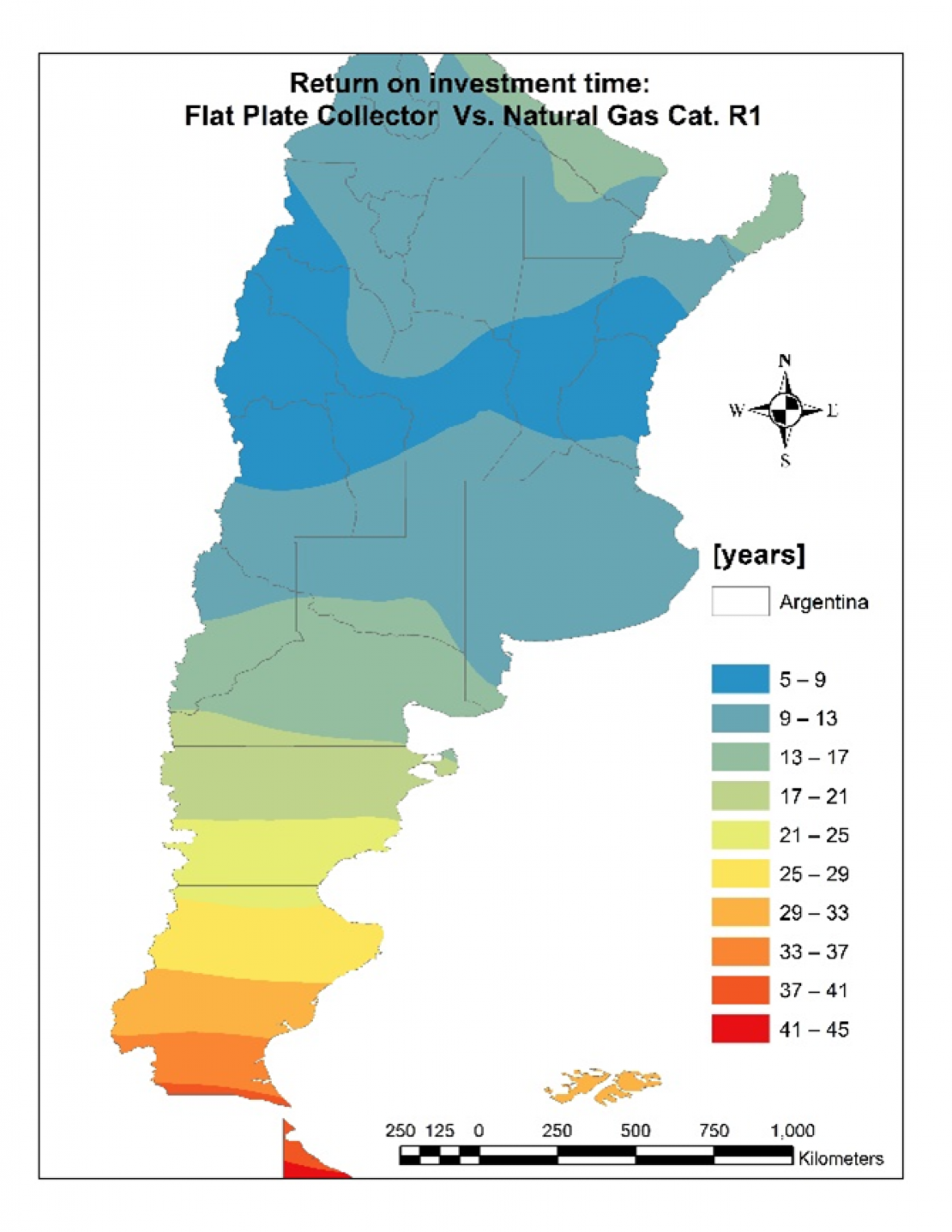

One recurrent question people ask before investing in a solar collector is the time necessary to recover the money invested (the payback period). To calculate it, we need to know how much solar energy the collector can transform into heat energy, so we need to know its performance. In turn, performance depends on the quality of the technology—including the materials used—and factors such as atmospheric temperature and solar radiation. Therefore, there are areas of the country where certain collectors have higher performance than others at a given time of year, such as winter, and the opposite condition can occur in summer, especially if we compare plate collectors and vacuum tubes. In addition, we need to know the cost of electricity or natural gas that one would save by installing a solar collector. Electricity and natural gas tariffs can differ greatly between the country’s 23 provinces, and sometimes even within each province. Based on these variables, we calculated the payback period for a flat plate collector and a vacuum tube collector for 118 geographical locations in Argentina. Then, using geographic information systems (GIS), we represent the payback periods in several maps, comparing scenarios for replacing the use of electricity or natural gas (Figures 2 in the gallery below). These maps show shorter investment recovery time for places with higher annual radiation and higher temperatures, but this does not occur in all cases due to the differences in energy tariffs. Our analysis shows that the choice of a solar collector for different areas in Argentina requires a specific analysis for each case, considering the performance of different technologies. The results also differ substantially depending on electricity and natural gas tariffs and dedicated subsidies. The current configuration of subsides discourages the diffusion of these technologies in many regions.

Figures 2: Return on investment time for flat plate and vacuum tube collector vs. natural gas and electricity

Distributed electricity: the challenging implementation of the new promotion law

With the enactment of National Law 27,424 "Regime for the Promotion of Distributed Generation of Renewable Energy Integrated to the Public Electric Grid", users of the distribution network, be they residential, commercial, or industrial, are enabled to generate renewable electricity for self-consumption, with surplus generation fed into the grid. The remuneration scheme is known as "Net Billing", which allows any energy generated that is self-consumed to be saved at retail price, whereas excess energy that is not self-consumed and instead fed into the grid is compensated in line with the purchase price of electricity in the wholesale electricity market.

From 2018 to now, the implementation of the law is advancing very slowly. As of May 2021, 12 provinces have adhered to the new Net Billing scheme, and a total of 152 distributors and electric cooperatives have registered. The regime presently has 468 user-generators with a combined installed capacity approaching 5 MW, while 340 users are in the process of connecting, representing approximately 4.2 MW of additional capacity. The commercial and industrial sectors represent 70% of the total installed capacity, while the residential sector represents 29%. Despite the multiple economic, social, and environmental benefits reported by the expansion of renewable DG, there are still economic–financial barriers, mainly related to the difficulty of buying the equipment due to high costs, combined with the generalized subsidies throughout the energy value chain, which discourage investment in solar panels and similar technologies. At the same time, certain economic incentives for DG provided for in the law have not yet been implemented.

As the local market develops, the cost of these technologies decreases through learning effects. However, the progressive growth of DG will depend on the knowledge and diffusion of these new technologies among the population, the local development of associated services, the availability of incentive mechanisms, the existence of a favourable macroeconomic and financial framework, as well as the evolution of electricity tariffs.

How and who can green energy microfinance help?

Despite dramatic improvements in both the performance and affordability of renewable energy technologies for DG, investment costs remain prohibitive for low-income populations. Especially in remote rural communities, access to energy is constrained by the limited ability to pay for the acquisition of such systems. Microfinance—which provides financial services to low-income populations usually excluded from commercial banking—has been proven worldwide as a vehicle to enable not only financial inclusion, but also energy inclusion. Through the delivery of loans for the purchase of clean energy technologies, microfinance institutions can play a key role in improving energy access, especially in remote areas where connection to the conventional energy grid would be technically challenging and/or cost-prohibitive.

The evolution of microfinance, in terms of the range of proven financing approaches, as well as in demonstrating a sustainable business model and strong infrastructure and establishing long-lasting relationships with communities in peri-urban and rural areas, makes it a good solution to overcoming the high initial investment costs of energy technologies. For this, partnerships between microfinance institutions (MFIs) and clean energy technology providers can be established, exploiting the expertise and abilities of each party, namely: delivery of financing (MFIs) and technology installation, training, and maintenance (technology providers). This strategy, also called the two-hand model approach, has been successfully implemented, for example, in Peru, where the MFI Cooperativa Fondesurco has been disbursing loans for solar thermal collectors with vacuum tubes for water heating in rural households, hostels, and hotels in Arequipa for almost a decade through its loan product: FondeEnergia.

While the microfinance sector in Argentina has experienced delayed and slower development, with smaller portfolios compared to other countries in Latin America, promoting and achieving the two-hand model approach there is not impossible. Indeed, an MFI in Argentina was one of the first in Latin America to take the initiative of combining microfinance and energy. In early 2005, there was already one microfinance institution, Emprenda, offering microloans for solar home systems (PNUD 2005). Since then, examples such as Banco de la Nación as well as the Instituto de Vivienda y Urbanismo de Jujuy (IVUJ) have offered programmes for delivering energy systems. Exploring this green microfinance approach, also called green inclusive finance, and tapping the potential of such partnerships provides an opportunity for the sector to transform the energy landscape of the country.

Some implications for public policy

Distributed generation has great potential in Argentina and should form part of a national strategy for a sustainable recovery in the wake of the COVID-19 pandemic. Investment in DG technologies can reduce energy bills for families and businesses while substituting a proportion of fossil fuel consumption. Renewables, in particular DG, have been overshadowed by the historical importance of fossil fuels, which have benefited from substantial public support, including large-scale subsidies. There is an urgent need to restructure the subsidy framework throughout the energy value chain, end incentives that preferentially favour fossil fuels, and allow more rapid diffusion of cleaner technologies. It is also essential to adopt policies to disseminate information on different DG technologies and also promote the development of microfinance institutions’ approach, thereby allowing the participation of low-income families.